Nvidia is driving the direction of global markets, commanding attention as central banks balance policy signals against fragile growth and critical inflation data. At the same time, Nvidia embodies the force of the AI revolution, symbolizing both technological progress and investor confidence.

This week brings an extraordinary overlap: central bank minutes from China, Australia, and Europe; inflation updates across the U.S., Australia, and Japan; and growth readings from Canada. Yet, through it all, Nvidia remains the anchor, serving as a barometer for whether the AI-driven momentum in equities can withstand macroeconomic uncertainties.

The Big Picture: Nvidia and AI Against Global Market Headwinds

Markets are caught between two powerful forces:

- Nvidia and AI innovation → fueling optimism, lifting valuations, and transforming industries.

- Central banks and inflation data → testing whether economies can maintain stability without reigniting price pressures.

In this environment, Nvidia’s performance is not simply a corporate update; it is a litmus test for global markets. Its GPUs are the foundation of AI, and its outlook is a proxy for the durability of one of the most important investment themes of the decade.

Monday: China’s Central Bank Sets the Week’s Tone

The week begins in Beijing with the People’s Bank of China (PBoC) managing liquidity through its Medium-Term Lending Facility.

- China’s backdrop: factory output sluggish, retail sales weak, property sector stagnant.

- Inflation data: consumer prices hovering near zero, producer prices in negative territory.

- Policy approach: instead of broad cuts, the PBoC deploys targeted tools—subsidized consumer loans and direct sectoral support.

Markets expect ~CNY 600 billion liquidity injection. A larger boost reassures risk sentiment; a smaller one risks deflation fears.

📌 Why it matters for Nvidia and AI: China is a key demand base and supply chain hub. PBoC’s cautious strategy reflects the fragility of global markets Nvidia operates within.

Tuesday: Australia’s Central Bank Minutes

Next, attention turns to the Reserve Bank of Australia (RBA). At its last meeting, the RBA cut rates to 3.60%—a small but symbolic step.

- Focus of the minutes:

- Did members consider a bigger cut?

- How do they weigh inflation risks vs. growth risks?

- What role do international risks (like China trade tensions) play?

- Market impact: A dovish stance weakens the AUD and supports equities; a more cautious tone gives temporary strength to the currency.

📌 Why it matters for Nvidia and AI: While far from Nvidia’s core, Australia’s monetary policy highlights how central banks everywhere are adjusting to uneven growth. These ripple effects contribute to sentiment that frames Nvidia’s market influence.

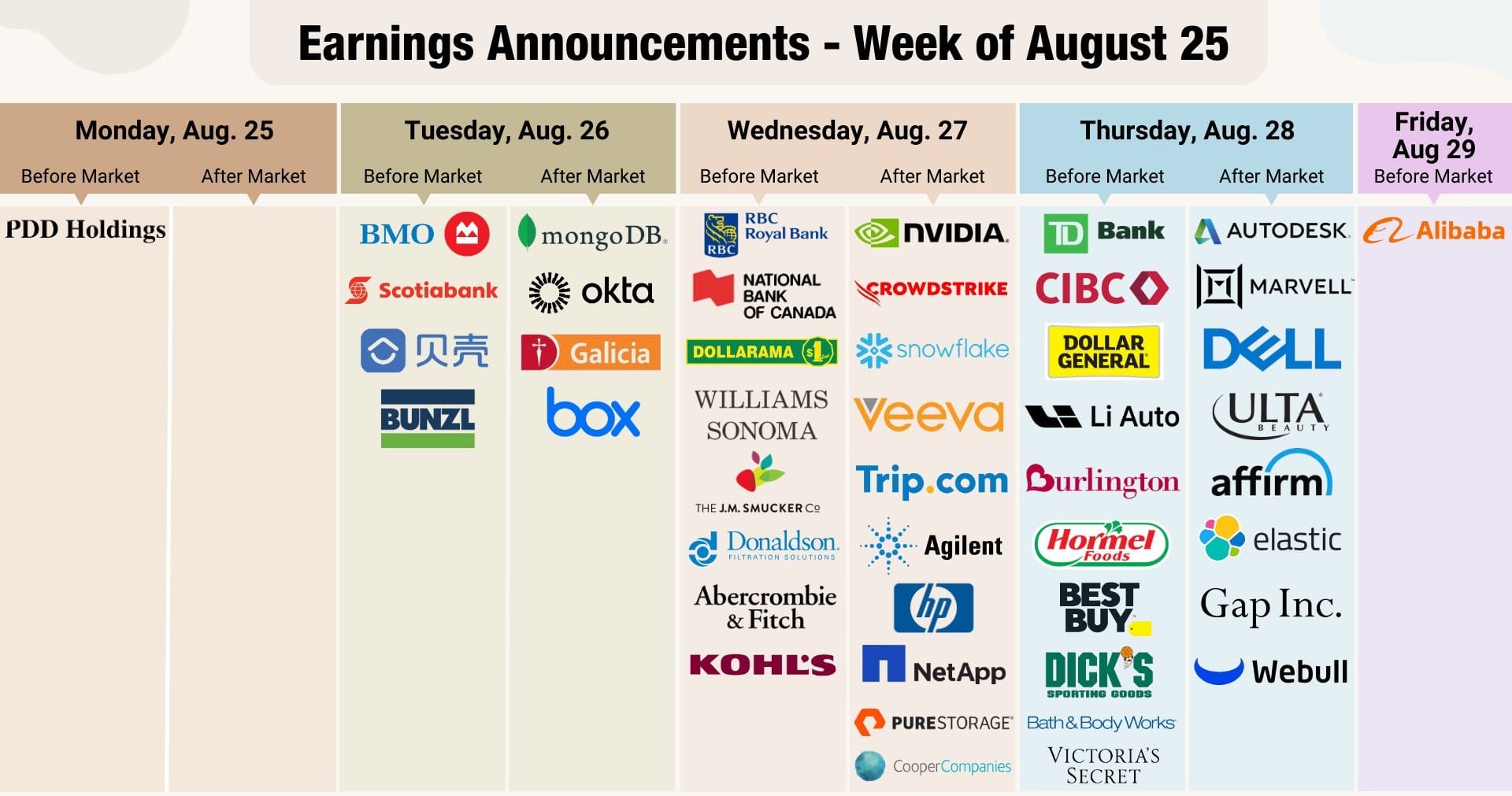

Wednesday: Nvidia at the Center of Global Markets

Part 1: Australian Inflation Data

Australia releases monthly CPI. Expected: +0.5% MoM, with annual inflation rising to ~2.3%. Electricity and energy costs remain pivotal drivers.

- Hotter print: reduces likelihood of further cuts, lifts AUD, pressures equities.

- Softer print: clears path for more easing, weakens AUD, boosts bonds and stocks.

This sets the macro stage for the day’s headline event.

Part 2: Nvidia Defines the Week

Nvidia dominates midweek, with results that transcend corporate earnings. Its GPUs power AI training, large language models, and cloud hyperscalers.

- Consensus expectations:

- Revenue ~$45.9 billion (+52.8% YoY)

- Data center sales ~$40 billion

- Margins ~72%

- Key uncertainty: China exposure and U.S. export restrictions.

- Bullish case: beats across metrics + confident guidance → Nvidia soars, lifting all of tech.

- Bearish case: beats but cautious guide → volatility, possible “sell the news” dip.

📌 Why it matters: Nvidia’s outlook dictates whether the AI narrative continues to outweigh inflationary headwinds in global markets. Its performance is seen as a proxy for the sustainability of technology-driven growth worldwide.

Thursday: European Central Bank Holds Its Line

The European Central Bank (ECB) minutes reveal more about its cautious hold. Rates remain at 2.00%, but divisions may exist within the Governing Council.

- Key issues in focus:

- Temporary vs. persistent inflation undershoots.

- Euro strength and its impact on exports.

- Trade tensions with the U.S.

- Market reaction: Unless divisions are revealed, the ECB stance is likely a non-event. But signs of hawkish dissent could pressure equities.

📌 Why it matters for Nvidia: While Nvidia drives tech sentiment, macro conditions in Europe shape investor allocation across global markets.

Friday: Global Inflation Data Wave

The week ends with a data deluge:

- U.S. Core PCE (July): Fed’s preferred inflation gauge.

- Softer print → supports rate cuts, weakens USD, lifts equities.

- Hotter print → delays cuts, strengthens USD, pressures stocks.

- Tokyo CPI (August): Leading indicator for Japan.

- Super-core inflation >3% → supports gradual BoJ normalization.

- Canada GDP (Q2): Growth near stagnation.

- Weak outcome → raises odds of BoC cut.

- Stronger print → offers temporary CAD support.

Together, these shape the macro backdrop Nvidia must contend with as a global growth leader in AI.

Conclusion: Nvidia as the Compass of Global Markets

This week underscores a unique interplay:

- Nvidia → the symbol of technological innovation and AI dominance.

- Central banks → balancing inflation control with fragile growth.

- Inflation data → the heartbeat of macroeconomic conditions.

- Global markets → the arena where these forces collide.

Volatility is inevitable. Yet, understanding how Nvidia’s leadership intersects with central bank caution and inflation data provides clarity for investors. In 2025, the central question is not whether AI matters—it is whether Nvidia’s momentum can continue to outpace the constraints of global monetary policy.