Executive Summary

As the final quarter of the year unfolds, the latest earnings season brings together a potent mix of corporate innovation, economic data releases, central bank decisions, and geopolitical maneuvering. The week of November 3–7, 2025, stands as a crossroads for markets: AI-fueled technology earnings meet high-stakes macroeconomic and political decisions across the globe.

Institutional investors are tracking the dual pulse of corporate performance and policy direction. From Palantir’s government analytics contracts to Robinhood’s retail resurgence, these earnings are not isolated updates — they’re microcosms of broader economic and technological transformation. Meanwhile, critical macro events — including OPEC-8’s output meeting, a landmark U.S. Supreme Court hearing on trade authority, and a series of central bank communications — set the stage for a potentially volatile but defining week.

This analysis serves as a strategic compass for decision-makers navigating interlinked market dynamics. It contextualizes corporate results within structural trends — artificial intelligence, energy transition, digital health, and monetary realignment — and ties them to the economic data that will move currencies, yields, and equities.

Part I: Corporate Earnings Spotlight

Innovation, Execution, and Market Expectations in Focus

The earnings season of early November highlights a diverse group of companies — each serving as a proxy for a different structural force in the global economy. From AI infrastructure to digital health and fintech democratization, these reports form the frontline indicators of both resilience and rotation in investor sentiment.

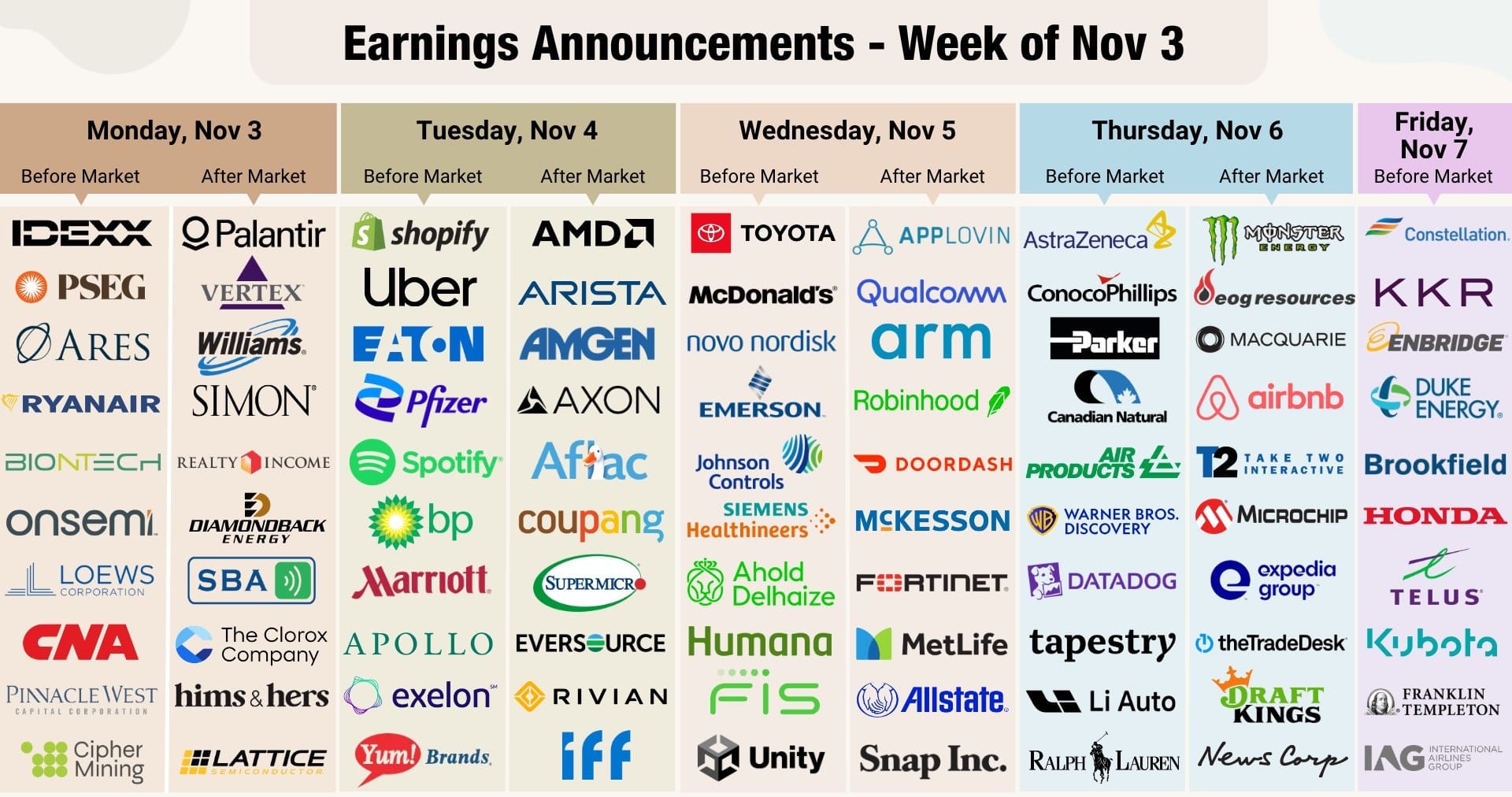

Palantir Technologies (PLTR): The Architect of Intelligence Infrastructure

Earnings Date: Monday, November 3, 2025 | Time: 4:05 PM ET

Consensus EPS: $0.17 | Revenue Estimate: $1.09B (+50.2% YoY)

Implied Volatility: 10.6% | 200-Day MA: $131.89 | Price Premium: +52.0%

Palantir has emerged as a core player in national security and commercial analytics, bridging classified operations with enterprise AI. Its Foundry and AIP (Artificial Intelligence Platform) deployments are becoming standard tools across defense, manufacturing, and logistics sectors.

Analysts remain optimistic — 63.6% expect an earnings beat — reflecting sustained demand for AI-powered decision systems. Contract wins with the U.S. Department of Defense, NATO, and leading industrials support its momentum.

Technically, the stock’s 52% premium above its 200-day moving average and declining short interest (-9.2%) highlight investor conviction. Should Palantir surpass the whisper EPS of $0.19 and expand its FY2026 guidance, the valuation could re-rate toward the $220–$240 range.

Strategic Insight: Palantir’s evolution from data integrator to operational decision platform makes it a bellwether for AI adoption across critical infrastructure.

Advanced Micro Devices (AMD): Powering the AI Compute Cycle

Earnings Date: Tuesday, November 4, 2025 | Time: 4:15 PM ET

Consensus EPS: $1.17 | Revenue Estimate: $8.72B (+27.9% YoY)

Implied Volatility: 9.2% | 200-Day MA: $138.76 | Price Premium: +84.6%

AMD remains at the epicenter of the AI semiconductor race. Its MI300X accelerators continue to gain ground against NVIDIA’s H100, while its Ryzen AI chips embed generative processing into consumer and enterprise systems.

With 78.4% of analysts anticipating a beat, and strong channel signals from Microsoft and Meta, AMD enters this earnings season with momentum. The 13% drop in short interest reinforces growing faith in its execution.

Institutional hedging remains visible through 26,951 contracts of $240 January 2026 puts, possibly guarding against supply constraints. Yet, given AMD’s historical 6.4% earnings volatility, the current implied move looks modest. A positive surprise and strong backlog commentary could lift shares toward $260.

Strategic Insight: AMD’s ability to translate AI opportunity into durable market share defines whether it remains a cyclical performer or a structural leader.

Hims & Hers Health (HIMS): Testing the Next Phase of Digital Health Growth

Earnings Date: Monday, November 3, 2025 | Time: 4:05 PM ET

Consensus EPS: $0.09 | Revenue Estimate: $583.68M (+45.4% YoY)

Implied Volatility: 15.3% | 200-Day MA: $47.34 | Price Discount: -4.0%

Hims & Hers stands as the face of consumer-centric digital health, balancing telemedicine, branded therapies, and e-commerce scale. Despite strong growth, investor sentiment is mixed — only 49.5% expect a beat amid rising acquisition costs and regulatory scrutiny.

Trading below its 200-day MA, and with increased put activity (30,859 contracts of $30 December 19 puts), traders are hedging for softness. Yet, improving gross margins or a new therapeutic category launch could shift sentiment sharply.

Strategic Insight: As digital health matures beyond pandemic-era growth, Hims & Hers must demonstrate it can scale profitably under tighter cost controls.

Robinhood Markets (HOOD): The Pulse of Retail Trading

Earnings Date: Wednesday, November 5, 2025 | Time: 4:05 PM ET

Consensus EPS: $0.51 | Revenue Estimate: $1.21B (+90.0% YoY)

Implied Volatility: 10.5% | 200-Day MA: $81.44 | Price Premium: +80.2%

Robinhood’s revenue surge underscores a new retail era — crypto rebound, product expansion, and trading volatility. With 74% of investors predicting a beat, sentiment skews bullish. However, short interest jumped 33%, signaling sophisticated caution.

Aggressive call buying of $155 November 7 options points to speculative momentum. Robinhood’s challenge is sustainability: converting short-term activity into long-term user value.

Strategic Insight: Robinhood’s transformation from app to financial ecosystem will determine if retail participation remains a lasting structural force.

Cipher Mining (CIFR): Industrializing Bitcoin at Scale

Earnings Date: Monday, November 3, 2025 | Time: 7:00 AM ET

Consensus EPS: -$0.08 | Revenue Estimate: $75.48M (+213.2% YoY)

Implied Volatility: 20.0% | 200-Day MA: $7.06 | Price Premium: +164.4%

Cipher represents the institutionalization of Bitcoin mining — strategic energy partnerships and next-generation rigs driving triple-digit revenue growth. Despite projected losses, 69.5% of analysts see an upside surprise.

Options flow is split — nearly 30,000 puts at $18 and 27,000 calls at $21.50, reflecting both hedging and speculative bets. Efficiency metrics — hash rate per watt and energy cost per terahash — remain crucial.

Strategic Insight: As Bitcoin’s 2026 halving approaches, Cipher’s operational efficiency will define its longevity and leadership in the energy-tech frontier.

Arista Networks (ANET): The Unseen Engine of AI Infrastructure

Earnings Date: Tuesday, November 4, 2025 | Time: 4:05 PM ET

Consensus EPS: $0.71 | Revenue Estimate: $2.26B (+24.8% YoY)

Implied Volatility: 11.2% | 200-Day MA: $110.22 | Price Premium: +43.1%

Arista quietly powers the digital backbones of AI and cloud hyperscalers. With 83% expecting a beat and short interest down nearly 20%, optimism is justified.

Its software-defined networking platform (EOS) delivers recurring high-margin revenue, and conservative guidance suggests potential upside.

Strategic Insight: Arista is the plumbing of the AI economy — its results serve as a leading indicator for global data center investment cycles.

Supermicro (SMCI): Balancing AI Demand and Execution Risk

Earnings Date: Tuesday, November 4, 2025 | Time: 4:05 PM ET

Consensus EPS: $0.28 | Revenue Estimate: $7.33B (+23.5% YoY)

Implied Volatility: 12.2% | 200-Day MA: $43.13 | Price Premium: +20.5%

Supermicro sits in a competitive AI server ecosystem, but margin compression looms. The company guided for $0.40–$0.52 EPS — above consensus — suggesting potential underestimation by the market.

Massive call buying (57,911 contracts of $52 November 21 calls) hints at speculative optimism, possibly tied to upcoming AI collaborations.

Strategic Insight: Supermicro’s ability to differentiate through design innovation and supply chain agility will determine its staying power in AI hardware.

Navitas Semiconductor (NVTS): Betting on GaN’s Next Wave

Earnings Date: Monday, November 3, 2025 | Time: 4:05 PM ET

Consensus EPS: -$0.05 | Revenue Estimate: $10.10M (-53.4% YoY)

Implied Volatility: 19.0% | 200-Day MA: $5.73 | Price Premium: +134.8%

Navitas, a pioneer in gallium nitride (GaN) power semiconductors, faces a sharp revenue drop but soaring investor enthusiasm. Despite only 36.4% expecting a beat, long-dated call activity shows faith in its EV and data center future.

Strategic Insight: Navitas represents the tension between technological promise and execution discipline — a dynamic common in emerging semiconductor cycles.

Uber Technologies (UBER) & Astera Labs (ALAB): Divergent Trajectories in Growth

Uber (Nov 4, 6:55 AM ET):

EPS $0.67 | Revenue $13.26B (+18.5% YoY)

Ninety percent of analysts forecast a beat, with attention on mobility margins and autonomous progress.

Astera Labs (Nov 4, 4:05 PM ET):

EPS $0.39 | Revenue $206.73M (+82.8% YoY)

Backed by AI infrastructure demand, 84.6% expect a beat, confirming its rise as an AI connectivity enabler.

Strategic Insight: Together, Uber and Astera symbolize the intersection of physical and digital infrastructure — one moving people, the other moving data.

Part II: Global Macro Calendar

Policy, Politics, and the Pulse of Economic Data

While earnings season captures headlines, the macro calendar for the week of November 3–7, 2025, is equally charged. A dense lineup of economic data releases, central bank announcements, and geopolitical events will set the tone for risk assets and investor positioning.

Sunday, November 2 – OPEC-8 Meeting & Daylight Saving Shift

The week opens with the OPEC-8 virtual summit, as Saudi Arabia, Russia, Iraq, UAE, Kuwait, Kazakhstan, Algeria, and Oman weigh whether to raise output by around 137 k bpd in December.

- Market Context: Inventories remain comfortable, yet demand visibility is clouded by slower industrial data in Europe and Asia.

- Political Underpinning: Crown Prince MBS’s forthcoming Washington visit encourages stability; neither side wants a renewed oil-price spike.

- Structural Signal: Brent’s move from contango to backwardation underscores near-term tightness but long-term caution.

Simultaneously, the U.S. daylight-saving reversion widens the London–New York gap to five hours, subtly altering global liquidity flows.

Monday, November 3 – U.S. ISM Manufacturing PMI & Treasury Refunding

With the U.S. government still under partial shutdown, official data releases are suspended, giving the ISM Manufacturing PMI outsize influence.

- A print above 50 after S&P Global’s flash 52.2 would reinforce resilience in factory activity.

- A sub-50 reading could reignite recession narratives.

Also on tap: the U.S. Treasury’s Q4 refunding announcement. With $590 B in borrowing needs and the Fed ending quantitative tightening December 1, the composition of new issuance will influence yield-curve shape and liquidity through year-end.

Tuesday, November 4 – RBA Decision & French Budget Vote

The Reserve Bank of Australia is expected to hold at 3.60 percent, though Governor Bullock’s language will be scrutinized for 2026 cut clues. Soft labor data contrasts with persistent inflation, leaving markets split.

In Europe, the French National Assembly votes on the Revenue portion of the 2026 budget. Failure could spark a no-confidence motion against Prime Minister Lecornu, widening the OAT-Bund spread beyond 80 bps and shaking EU fiscal cohesion.

Wednesday, November 5 – Supreme Court Tariff Hearing & ADP Report

In Washington, the U.S. Supreme Court hears Trump v. International Trade Commission, testing the constitutional limits of presidential tariff powers under IEEPA. A ruling curbing executive authority could force refunds on prior duties and reorder global trade assumptions overnight.

With official labor data offline, the ADP employment report becomes the only timely proxy. Early pilot data showing +14,250 jobs will be dissected for wage and hiring momentum, shaping expectations for the December FOMC meeting.

Thursday – Friday: The Central Bank Quartet & Key Economic Reports

Bank of England (Thursday)

- Expected to hold rates at 4.0 percent, though a 6–3 split vote could signal dovish drift.

- Markets watch Governor Bailey’s remarks for hints about early-2026 easing ahead of the U.K. budget.

Norges Bank (Thursday)

- Likely steady at 4.0 percent; inflation-adjusted real rates remain restrictive.

- Any reference to Q2 2026 cuts would weigh on the krone.

Canadian Jobs Report (Friday)

- Forecasts point to modest hiring after last month’s decline.

- The data will test labor resilience amid U.S.–Canada trade friction and soft energy exports.

China Trade Balance (Friday)

- Analysts expect a $101 B surplus, though data quality is questioned following the Xi–Trump détente.

- Any export recovery would validate Beijing’s incremental stimulus efforts.

Economic Data and Market Interdependence

Each release interacts with corporate earnings in real time:

- A strong U.S. PMI or upbeat ADP print could validate optimism priced into AI-heavy equities like AMD and Arista.

- A dovish BoE or soft Canadian jobs figure could steepen global yield curves and shift portfolio allocations toward growth stocks.

- OPEC’s cautious stance feeds directly into energy equities and inflation-expectation trades.

This convergence exemplifies how economic data is no longer background noise but a market-moving catalyst intertwined with the corporate narrative.

Conclusion: Synthesizing Signals in a Fragmented World

The confluence of earnings season, economic data, and geopolitical recalibration marks this first week of November as one of 2025’s defining junctions. It is not just the volume of news that matters but its interconnected architecture.

- A Palantir earnings beat could validate defense-tech valuations precisely as Supreme Court tariff rulings reshape trade expectations.

- A dovish Bank of England stance may clash with fiscal retrenchment in France, amplifying European dispersion trades.

- AMD’s AI momentum could offset weak macro signals, underscoring technology’s new defensive role in portfolios.

For investors, success in this environment hinges less on speed and more on systemic awareness—seeing how fiscal, monetary, and technological currents reinforce or contradict one another.

Earnings season is no longer an isolated quarterly ritual; it is a live diagnostic of the global economy’s adaptability. Central banks may pause, politicians may pivot, but capital will continue to seek clarity in data, policy, and execution.

In an era defined by overlapping crises and innovations, the ultimate edge lies not in prediction but in preparation—reading connections where others perceive only noise.